The Company’s operations in 2015 were significantly impacted by the following key macroeconomic factors:

- global and national economy growth rates;

- RUB/USD FX rate and inflation rates in Russia;

- global oil and gas prices.

GLOBAL AND NATIONAL ECONOMY GROWTH RATES

The global economy growth rates slowed down in 2015 to 3.1 % YOY (3.4 % YOY in 2014) due to a slowdown in the economic dynamics of developing countries to 4 % YOY in 2015 4.6 % YOY in 2014). Such slowdown was due to the reduced scope of commodity products export, slowed down growth rate or reduced amount of investments and consumption rates.

The growth rates of developed economies (ОECD) being key consumers of resources in the global market (USA, Japan, and Eurozone countries) in 2015 increased by 1.9 % YOY (1.8 % YOY in 2014).

The economic situation in Russia in 2015 was affected by worsening external trade conditions mostly triggered by decreasing oil prices and continued economic sanctions imposed by EU and the United States. Russian GDP in 2015 decreased by 3.7 % YOY.

According to the forecast of the International Monetary Fund (IMF) as of January, 2016, future global GDP growth rates will be faster and will reach 3.4 % YOY in 2016 and 3.6 % YOY in 2017. Growth rates in developed economies are expected at 2.1 % YOY in 2016 and 2017 and those in developing countries, at 4.3 % YOY and 4.7 % YOY respectively. According to the IMF forecast, 2016 GDP of the Russian Federation is to decline by 1 % YOY (according to the forecast of the Ministry of Economic Development — by 0.7 %); in 2017 the economy is forecasted to grow by 1 % YOY.

ENERGY PRICES, RUB/USD FX RATE AND INFLATION RATES IN RUSSIA

2015 was characterized by the growing imbalance in the global oil market with supply significantly exceeding demand which was a key factor for a decline in the global oil prices in 2015 by more than 47 %.

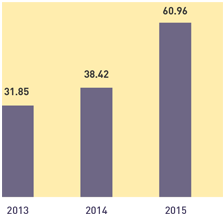

In the context of low global oil prices, Russia, as well as many other countries exporting oil, experienced the devaluation of its national currency. RUB devaluation against USD based on 2015 results amounted to 37.0 % (versus 17.1 % in 2014).

Inflation in Russia remained high: the consumer price index and producer price index in December 2015 was at 12.9 % and at 10.7 % year-on-year, respectively.

The transportation expenses of oil companies in Russia increased significantly in 2015. The indexation of Transneft tariff rates for main oil pipelines was at 6.5 % YOY and at 7.5 % YOY for oil transportation to eastern regions via the ESPO pipeline. Government-regulated tariff indexation, duties, and charges for cargo transportation and infrastructure services during shipments by Russian Railways in 2015 amounted to 10 % YOY.